|

| Dürer, Melancholia I, 1514 |

Given that it's been about 5 years since Walker first laid out a basic outline of the current crisis, it's time for an update. This initial post revisits that thesis while laying the groundwork for a second part, which looks at the political formations that have emerged in response to the slow, fitful death of neoliberal society. The idea is to clarify the context in which we act by understanding the present as history. Without further ado, let's get into it.

Hic Rhodus, hic salta!

***

Recent years have not been kind to received wisdom. Orthodox economists in the government and the academy complacently assured us for decades that the twin motors of innovation and efficient markets would drive endless economic growth, benefiting everyone. These very two factors then came together through the wondrous laboratories of the derivative markets to nearly blow the global economy sky-high in the crash of 2008. The ordeal came as a total shock to the lizardly Alan Greenspan, the fallen oracle of neoliberalism, for whom the whole disaster was a kind of sentimental education in which his “whole intellectual edifice collapsed.” Greenspan’s maudlin mea culpa before an equally clueless congressional committee shortly after the crash was a perfect image of the intellectual bankruptcy of the technocratic elite, a kind of show trial whose effect was to reaffirm the established dogma through the appearance of questioning it.

After that, we were informed that the recent unpleasantness, while unfortunate, was an inexplicable anomaly that sprung upon us, Spaghet-like, and that no one saw coming (though of course quite a few people did). A swift government bailout of the imperiled banking sector was necessary to place the economy on a strong foundation of renewed growth, but once it was done things should gradually return to normal, the story went. Since then the ensuing “recovery” has been rather less than robust. Declining unemployment in the U.S. is the one stat that looks quite good at a glance, thus the mainstream media’s dutiful adherence to it as main indicator of the health of the economy. But the official estimate systematically underestimates its real level, which is considerably higher. In any case wages for those who are employed are still stagnating, with income inequality skyrocketing since the crash, and overall growth levels as measured by GDP remain depressed.

The underwhelming recovery is all the more remarkable given the unprecedented monetary policies carried out by the world’s central banks. Once it became clear that a swift revival of the economy was not forthcoming, with productivity, investment, and inflation all remaining depressed, the need for some kind of intervention to kickstart the process became evident. Since sound macroeconomic sense ruled out of bounds from the start any major state spending program in the classical Keynesian sense, governments and central banks conjured up a different program. The idea would be for the Federal Reserve to sluice hundreds of millions of dollars of “money” into the financial markets via the purchase of bonds - particularly U.S. Treasuries - and the “toxic” (non- or underperforming) assets that still were clogging banks’ balance sheets. By driving down interest rates and flooding the markets with liquidity, “Quantitative Easing” would prime the pumps of investment, new employment, innovation, and job growth that would finally set the gears in motion for a genuine recovery. The resulting conjuncture, which has defined the political terrain since, is based on a strange paradox of extreme profligacy in state monetary policy, on the one hand, and equally extreme fiscal austerity on the other.

The results have been at best mixed. Everywhere this program has been implemented - the Federal Reserve, the European Central Bank, the Bank of Japan, and, in a different form, the Bank of China - the outcome has been underwhelming, with productivity, profitability, and overall growth rates remaining well below “potential.” As it became clear that this wasn’t cutting it, governments began to turn to negative interest rates on short-term deposits, meaning commercial and investment banks must now basically pay a fine to store their money at the central bank. Again, the expectation was that this would spur investment to kickstart the global economy, but - again - it hasn’t really worked. A stubbornly lukewarm recovery in the U.S. continues to puzzle mainstream observers, while Japan and Europe remain mired in stagnation. The end result is a sort of economic limbo in which the advanced economies of the Global North are always on the verge of “taking off,” but never quite reach escape velocity. In the meantime, world capital markets - the innovative, dynamic sector that supposedly powers the global economy - navigate a true terra incognita, a set of policies and conditions that capitalism has never seen before and whose ultimate result, frankly, is known to no one.

Light Fuse, Get Away

I’m not the first to have pointed out the ambiguous record of these monetary programs, of course. But the sheer weirdness of it all has yet to be fully appreciated. Despite nearly 5 years of pumping untold billions into global financial markets through the firehose of QE, inflation remains very low if not nonexistent in Europe and North America. “Disinflation” has been the buzzword of late, but it has become clear that this is really just a euphemism for stubbornly persistent deflationary pressures that won’t go away no matter the size of the monetary intervention. Likewise, negative interest rates have yet to put even a small dent in the problem, as overall investment levels remain depressed. It increasingly looks like the central banks are merely pushing on a string. No doubt bien-pensant thinking around the technical issues of monetary policy did not expect this to be the situation a full 7 years after the economic “recovery” began, but here we are. Basically, increasingly extreme monetary measures are yielding increasingly meager economic results. As a simple comparison, it’s getting harder to avoid the impression that the patient’s vital signs are fading despite the doctor’s ever more desperate attempts to resuscitate it.

If all this sounds disconcerting, it should. While most neoclassical economists and technocrats continue to assume that a healthy combination of technological innovation and “structural reform” (fiscal austerity) will restore the productive potential of the ailing economies of the Global North, a few mavericks have broken ranks with the standard view. Former chief economic advisor to the Clinton administration, Larry Summers, is among these apostates, warning of the dangers of a long-term “secular stagnation” of the world economy unless a different approach is adopted. In fact a handful of elites at the top of the global financial system, including Christine Lagarde of the IMF, have been vocal critics of austerity economics, urging a more “inclusive capitalism” as the wave of the future. This arguably aligns them with contemporary post-Keynesians, who continue to advocate a much stronger, larger fiscal stimulus program carried out by national governments as the only solution to the current malaise. All agree that some major break with received thinking is necessary.

More recently, the critique of “financialization,” long a preoccupation of the left, has decidedly entered the mainstream discussions. In an exceptional piece of reportage - in Time magazine of all places - Rana Foroohar has packaged its basic parts in an admirably clear argument: whatever the financial sector may once have been, it has now metastasized into a bloated casino of recklessness and short-termism, parasitically extracting profits from the “real economy” while contributing very little to nothing in return. As Foroohar well knows, and as some on the left have been arguing for some time, the failure of the enormous monetary stimulus programs to have any real effect on GDP or growth rates throughout the advanced economies is largely due to the way it is swallowed up by the financial sector before it can have any such effect. Tidal waves of liquidity are pumped into the banking system through the central banks’ policies with the expectation that this will kickstart lending and productive investment; instead, it simply feeds stock buybacks, big mergers and acquisition deals, larger dividend payouts, higher executive pay, and, of course, it prompts “strategic adjustments,” i.e. downsizing and layoffs. This “asset-price Keynesianism,” to use Robert Brenner’s phrase, does several things: it drives up share prices, stoking a bullish bonanza in the stock market along with all its unavoidable speculative excesses; it progressively cheapens borrowing costs, as demand for corporate bonds rises along with equities, further feeding the debt binge; it powers ever more feverish bouts of speculation, and ever more “creative” types of derivative contracts; and it drives skyrocketing levels of inequality even higher, as the paper wealth of the wealthy and corporate elite goes through the roof, while wages for the vast majority of workers don’t budge.

The desperate improvisations of the world’s central banks have kept the ship of capital afloat, but at huge cost and not without producing new structural contradictions of their own. From the beginning, central bank policies have played a key role in the speculation-fueled bubble dynamics that have powered every boom-and-bust cycle since the early 1980s. Their centrality in this financial regime, which can only reproduce itself through such cycles, is the principal source of their enormous political and social power.

The introduction of the wildly inflationary monetary programs about 5 years ago has induced an even tighter integration of the central bank hubs with the world financial system - so tight, in fact, that it may no longer make sense to refer to “markets” in the financial industry, if markets are supposed to include some meaningful type of competition. Instead, since around 2012 financial networks and the central banks have seemingly fused into some new, hybrid monstrosity.

Rather than banks and firms competing for investors, central banks now offer unlimited liquidity. Whenever they suggest that unlimited funding may not be permanent, or that interest rates may increase because the economic outlook is improving, the markets tend to swoon and begin to tank, threatening billions in losses; conversely, whenever they report that the economy is doing badly, and so the fount of cheap credit will continue, the markets go into a manic frenzy, rallying and inflating asset values. The "markets" now just move in unison: up if the news is bad, down if the news is good. Locked in a kind of catch-22 pattern, the central banks basically can't talk about the economy improving - and thus monetary tightening - without triggering the kind of market chaos and widespread devaluation that their own policies are meant to prevent. This wouldn’t be happening if the waves of liquidity flowing into the financial system were actually creating the large-scale capital investments, rising employment, and “job creation” the policies were meant to bring about in the first place.

It might feel natural here to bemoan the useless, outlandish excesses of finance in the name of the “real economy,” the true source of value that is being suffocated by the invidious rentierism of parasitic bankers. This would be to fall back into the delusions of the pundits who constantly fret about whether economic “fundamentals” are sound - or, conversely, of leftists who argue for “breaking up the banks” to fight the power of finance capital. As I’ve argued at length elsewhere, when the logic of financial mediation penetrates the very core of capital as a world-spanning mode of production, to strictly distinguish between a productive “real” economy and its superfluous, purely speculative excess is to reify their historical interconnection. Following Marx’s analysis in Volume II of Capital, it is to assume a one-sided perspective from either the standpoint of productive capital or money capital, but without bringing them together within what he calls the whole circuit of “industrial capital” - it is to fall into the simple, static opposition between productivism and finance. This reification is typically deployed on the left in a nostalgic bid for the lost object of Fordist manufacturing, sustaining the fantasy that, for example, one need only roll back financial power by downsizing and better regulating banks and corporations for an idyllic, competitive society of small businesses, productive factories, and a strong welfare state to return to the U.S. It is shared by orthodox economists, who exclude finance from their macroeconomic models of national economies. And in reactionary circles, of course, tirades against the predations of finance capital from the standpoint of “productive” industry have a dark history, which incidentally is experiencing quite the revival of late.

The question is not whether finance is absorbing an ever greater share of the social product. Nor is it the false dichotomy that says a choice must be made between national manufacturing productivity, on the one hand, and global trade on the other. The question is why a ravenous financial sector is actually integral to this social formation, and the opportunities, constraints, and dangers this presents for our politics.

Inflection Point

Mainstream discussions of the economy are almost always oblivious to the fact that a bloated, metastasizing financial system is not a sui generis phenomenon. Its economic centrality and political power in the U.S. are both expressions of a wide-ranging structural transformation in the nature of capitalism itself, a global process whose political and cultural consequences have been analyzed extensively on this blog and elsewhere. Without a full rehearsal of that analysis, its basic upshot is that the hyper-financialized, crisis-ridden form of growth that has driven accumulation since the early 1980s reached its historical limit in the dramatic meltdown of late 2008. In this view, the crash and ensuing slump marked the “signal crisis” of that mode of production, to use Giovanni Arrighi’s term, which spelled the beginning of its end. The conclusion then was that the global economy was essentially on its last legs following that disaster, and that a general crisis of capitalism was on deck. But as Marx says somewhere, no mode of production can be finally superseded until all of the productive forces within it have been exhausted.

It has become apparent, retrospectively, that the bizarre monetary experiments of the central banks have been mostly successful in maintaining a sufficiently manic level of liquidity in global markets, and preventing another system-wide seize-up, for the last half-decade. Yet in achieving increasingly meager results through increasingly drastic measures, Bernanke, Yellen, Draghi, Kuroda, and the rest of the gang are bringing the distended, dysfunctional regime of economic governance inaugurated by Paul Volcker in the late 1970s and perfected by Alan Greenspan to a fittingly absurd conclusion.

This technocratic wizardry seemed to work for a time because it expanded the supply not just of money, but of what the anthropologists Edward Lipuma and Benjamin Lee, among others, call “abstract risk.” Abstract risk is the universal equivalent for exchange that is generated through financial derivatives and allows for the commensuration of any type of asset with any other, no matter how different they may be. In the absence of a metallic standard, fixed exchange rates, or economic coordination, they argue, abstract risk serves as the form of connectivity linking radically different and otherwise incommensurable currencies, commodities, and cultures together into a common network of valuation. It is essentially the source of liquidity, and is thus at the heart of globally networked, hyper-financialized capitalism. When they create money out of thin air, the central banks are essentially “manufacturing” this strange meta-commodity, pumping it into the world’s financial and banking systems like some gigantic iron lung. They pour fuel into the furnace of derivative finance, drastically cranking up the velocity of circulation and cutting down the turnover time of capital. The expansionary cycles of recent years - like those before them - have manufactured an illusion of accumulation by multiplying claims on existing assets, generating claims on those claims, and on and on in the spiraling vortex of the derivative form. They are the culminating act of the central banks as a force of production in their own right. But their success, which can only be seen as marginal at best, has come at a rather dear cost, exacerbating inequality, further chaining the fate of the global economy to the blind frenzy of the financial system, and baking in the inevitability of another huge bust sure to come at the end of the current, precarious boom.

This program, such as it is, had managed for some time to maintain a simulacrum of the general pre-2008 economic geography: mainly services, retail, and debt-fueled consumption in the G7 countries, with reduced but still significant manufacturing production, particularly in Germany and Japan; and higher rates of fixed capital investment and accumulation in the leading countries of the Global South, particularly in China, now fueled by an influx of speculative “hot money” from western banks. But despite this temporary fix, actual capital accumulation has been slowing drastically in the G7 countries, while the much celebrated BRICS, whose economic ascendancy was once thought to herald the future of global capitalism, are all struggling if not floundering in outright depression. Beneath the surface, various observers have been tracking steadily slumping profits in international capital, while a creeping descent in productivity in the U.S. recently accelerated, dropping sharply even into negative territory - the first contraction of productivity in the U.S. in 30 years. The U.S. economy, supposedly the sole “bright spot” in a stagnant world economic system, has - for the moment - essentially stopped growing.

|

| Figure 1. Source: Brookings Institution |

|

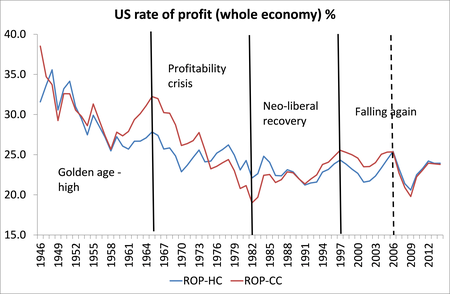

| Figure 2. Source: Michael Roberts |

The gradual but seemingly inexorable plunge in productivity and profitability - almost as if there were a long-term tendency like that - augurs something very ill for capitalism in the current moment. Abysmal productivity rates confirm that profits are not low because they’re being productively reinvested, powering accumulation. They are low because the finance-centered pattern of growth pursued for the last half-decade seems to have run its course without boosting productivity in the least. It pleased the stock markets by creating some impressive quarterly earning reports for a few years, as firms plowed their surpluses back into the financial system rather than accumulating capital. And for a while runaway credit growth and the expansion of financial assets of all kinds could sort of drag other areas of the economy along with it, as it gradually seeps into services, real estate, construction, start-ups, and other low-productivity industries that tend to be attractive to speculative capital. But the magic tricks of financialized, non-productive growth can only be performed so many times before their effect wears off. And in any case it can only last as long as the glaring contradiction between financial expansion and shrinking productive investment remains obscured. Once it becomes clear that the upward movement of the markets is due not to “strong fundamentals,” but to an empty charade concealing fading productivity and dwindling profitability, the reckoning will be severe. It’s most likely only a question of time until that happens, but if and when it does, it promises to reveal what happened in 2007-2008 as a mere prologue to the real catastrophe.

No comments:

Post a Comment