Despite the differences between the US and Europe in the average

citizen’s experience of life, there have been some striking similarities in the

development of deeper structures in the world’s two biggest economies since the advent of neoliberalism. This

indicates that the crisis in Europe is not merely a result of “contamination”

from the American credit crisis of 2008, as many Europeans initially argued.

Yet neither is it a result of solely European problems of excessive spending or

lagging competitiveness, as many Germans and Americans believe. It is, rather,

a constituent part of the ongoing crisis of global neoliberalism.

It’s much harder to get a good grasp on these developments in Europe because aggregated statistics are not readily available before the advent of the eurozone and because exchange rates introduce some methodological problems, not to mention that the most important national economy used to be two different countries. This is further

complicated by the UK’s decision to stay out of the single currency, leaving

one of the key economies of Europe out of eurozone statistics. I’ve had no luck

finding continuous time series that could give us the kind of elegant graphical

picture of trends from Fordism to neoliberalism that we get for the US, so a

more impressionistic jumble of charts for individual countries will have to

suffice.

At least in France, this has been accomplished by the same kind of wage suppression as in the US. Here we see that wages rose with productivity in the Fordist period and diverged sharply with the advent of neoliberalism (I was unable to locate similar data for other countries stretching back far enough, though the rising share of value going to capital indicates that this is a common phenomenon throughout Europe):

and France (the blue line is debt as a percentage of GDP):

First, like the United States, growth in productivity has declined substantially from

the rapid increases of the Fordist era (these charts are based on data from

Eckhard Hein and Artur Tarassow, “Distribution, aggregate demand and

productivity growth: theory and empirical results for six OECD countries based

on a post-Kaleckian model”, Cambridge Journal of Economics (2010) 34, p.

728)

As can be seen, the collapse in productivity growth has been even

more marked than that in the US, though the American (and British) numbers are padded by the

tremendous amounts of fictitious capital its financial sector has generated since the mid-90s. As in the US, in order to maintain profit rates European

corporations have captured a rising share of society’s production of value since the neoliberal

rupture. The dotted lines below show the share of GDP taken by profits in A)

Germany, B) France, C) Netherlands, D) Austria, E) UK, F) US; the straight

lines show the evolution of productivity growth. Clearly, this development too

has been more striking in Europe than the US (from Hein and Tarassow, p. 746):

At least in France, this has been accomplished by the same kind of wage suppression as in the US. Here we see that wages rose with productivity in the Fordist period and diverged sharply with the advent of neoliberalism (I was unable to locate similar data for other countries stretching back far enough, though the rising share of value going to capital indicates that this is a common phenomenon throughout Europe):

|

| Source |

Just as in the US, squeezing the enormous consumer market that had

emerged under Fordism produced two significant problems: the prospect

of mass unrest if living standards stagnated, and the question of how to

actually sell the economy’s growing output if consumers’ incomes were not rising.

And just as in the US, increasing levels of debt was the solution to both

problems. But – and this is the basis of many of the observed differences in

national life between the US and countries in Europe – the burden of this debt

was taken up primarily by governments in Europe while individual borrowers were more important in the

US (graph based on data supplied here):

In other words, broadly speaking, debt in Europe financed public

goods that were equitably distributed (healthcare, public transit, welfare programs) while in the US it financed McMansions and SUVs. But in both cases,

the issuance of this debt represented a claim on future production that could

not be made good because productive outlets for investment in the economy were

drying up.

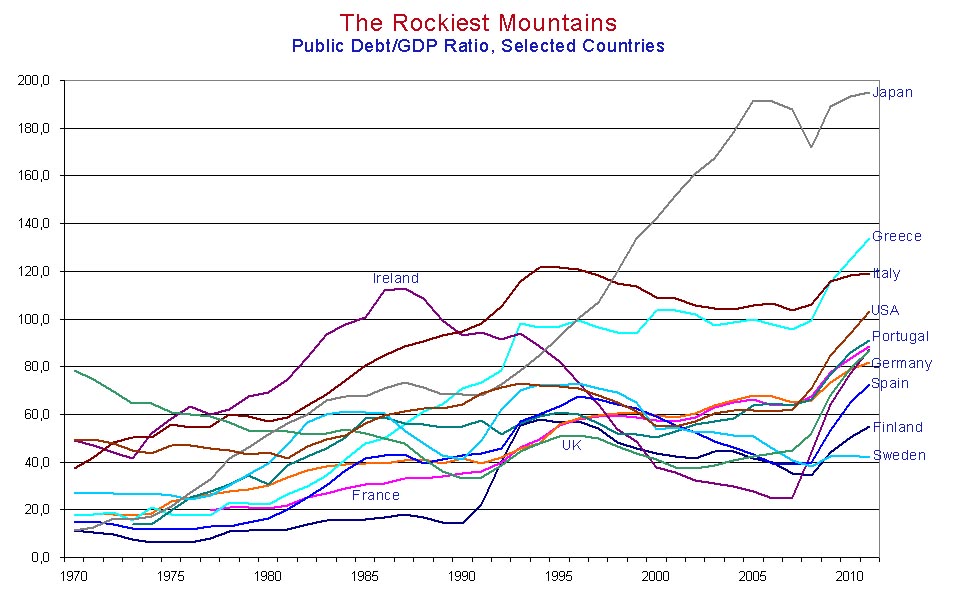

We can see the sharp increase in government debts during the

neoliberal period here:

|

| Source |

{kind=link}

And, since that graph is a bit messy, here are individual ones for

Italy:

|

| Source |

|

| Source |

{kind=link}

The rise of private debt in Europe, however, was also a significant development:

Finally, just as in the US, the financial sector as a whole has become more and more important in the European economy:

This graph overstates the significance of finance in the eurozone considered as a whole since French and German banks account for more of the sector than those of the other major economies, but the trend is clear. And with the exception of Greece and Italy, the speculative bubbles (mainly in real estate) that the European banks inflated in the UK, Spain, Ireland, and Iceland have been central to the seemingly national crises that have unfolded one after the other.

|

| Source |

|

| Source |

It goes without saying that there are many differences between the

US and Europe that complicate this basic picture considerably, and I hope that

we will have a chance to explore these further. But what I want to argue is that

in a very fundamental way, the two economies (and not just the economies, but

the politics and culture as well) have developed in a similar direction because

they both adopted neoliberal social forms in response to the crisis of the

1970s.

It can hardly be denied that the American version of neoliberal

social forms was far more extreme, marking a much sharper break with Fordist

social forms than in Europe (with the exception of the UK). The partial

survival of Fordist forms in Europe, including stronger unions, a more robust

sense of the public good, and a less complete exposure of people to market

insecurity, goes a long way toward explaining why life in Europe has been so

much less savage there over the last three decades. It also accounts for Europe’s

consistently slower rate of growth. These social forms were well adapted to the

Fordist moment, but they were less successful – at least in capitalist terms – under

neoliberal conditions.

Even so, precisely because neoliberalism was implemented in an

extreme fashion in the US, the dysfunctions of the system were most pronounced

there, and it was there that the crisis of neoliberalism exploded. Yet Europe,

as a part of the unitary global order of neoliberalism, was not immune. And because its underlying model of growth was the same as in the US –

consistent investment levels maintained only through corporations taking a rising share of

value, with the problem of realizing value being

solved through increasing debt – the crisis paralyzed prospects for

future growth.

This crisis of growth has now assumed the form of a crisis in government finances because of the peculiar monetary system that mediates the

euro. But the basic economic structures of neoliberalism remain in place, and

the ideologies generated by the neoliberal era continue to block any initiatives

but those that will deepen the crisis. It’s too soon to tell

if the crisis in Europe will finally undo the short-term fixes that have

forestalled complete global economic collapse. But even if the German

government and ECB finally decide to save the currency before it’s too late,

the crisis of growth will continue.

This is very helpful. I'd like to see you go further on the idea that the continental model of neoliberalism relied on sovereign debt as opposed to consumer debt. I wonder if there's a way to quantify consumption in such a way to show more clearly that the increase in debt was causally linked to lagging demand. You might be able to use import/export numbers combined with gross output numbers to quantify consumption to show an increase in or at least constant aggregate consumption while the proportion of spending moved toward debt or away from individual consumers and toward states. There might problems with this approach both in getting the numbers and in the fact that you might not be able to show that public consumption increased over the last 30 years to make up for some household consumption deficit.

ReplyDelete